Business rates experts at commercial property firm Colliers International have welcomed Scottish Finance Secretary Derek Mackay’s adoption of the Barclay Review but say details and dates are urgently needed to help landlords and occupiers make decisions.

With 100% rates relief potentially available for a year on both new and improved premises, knowing the start date and the rules for qualifying is essential for businesses to make commercial decisions. This could either significantly reduce their occupational costs or stimulate investment and redevelopment by landlords.

Louise Daly, Associate Director – Rating of Colliers International in Scotland, said: “Mr Mackay has gone above and beyond the Barclay Review by adopting its additional suggestion – which fell outside of the cost neutral remit of the report – to move annual poundage increases from the RPI to the CPI inflation measure. This was essential in order to match England and ensure businesses aren’t disadvantaged by choosing to locate north of the Border. This still means that ratepayers will see a 3% increase next year, which is in excess of the levels capped at 2% in previous years, in an effort to remain consistent with England. While, on the face of it, a positive step and one that industry has called for, it would be better for ratepayers to receive a set uniform business rate across the term of the Revaluation when the rateable values come into effect. This would enable businesses to budget more accurately and with certainty over their liability.

“Of course, the promised adoption of the Barclay Review’s key recommendations on rates relief are also welcome, but landlords and businesses need to see a fully detailed implementation plan, with specific information on how these reliefs will apply and, crucially, dates.

“Proposed empty property relief for new commercial buildings, for example, is expected to start on April 1. But what happens to businesses signing leases or moving in before that date? The difference between paying full rates and getting 100% relief for a year is simply too significant for any potential occupier to ignore.

“In today’s speech, Mr Mackay also seemed to go beyond the recommendations of the Barclay Review, when he suggested this relief should also apply to improved premises. While this chimes with the Government’s drive to encourage investment and development, creating better quality stock onto the market, landlords will naturally be very curious to see what level of improvement or refurbishment is required in order to qualify for this relief.”

The Scottish Government had promised details of its changes to rates as a result of the Barclay Review by the end of this year. Ms Daly said that while reliefs encouraging new and improved property should eventually have a positive effect by making much needed premium business accommodation available, it remained to be seen what effect it would have on older stock which will become even less attractive to tenants.

She added: “On the face of it this has been a very positive statement. One final issue that remains to be seen is just how consistently the rules on relief will be applied across Scotland. Hopefully we will see a country-wide approach that gives clarity to landlords and tenants, rather than a situation where some billing authorities are less eager to grant relief than others. This could be a problem when it comes to refurbishments, in particular, as it seems inevitable that a judgement will have to be made as regards what level of improvement qualifies for relief – for both landlord and tenant.”

Colliers International has welcomed assurances by ministers that the Scottish Government intends to implement the vast majority of the recommendations of the Barclay Review on Business Rates.

Louise Daly, associate director of rating at Colliers International in Scotland, said: “When the Barclay Review was published last month, we backed it strongly and said the Government must implement it swiftly, not simply focusing on revenue raising aspects or miss a golden opportunity to create a significantly fairer Business Rates system. Although ministers are understandably and rightly wary of implementing some measures designed to raise revenues lost elsewhere, the indication seems to be that all the core measures designed to make for a fairer business environment in Scotland will be adopted, and we wholeheartedly welcome that.

“The remit of the Barclay Review was that it had to be revenue neutral, but from a point of view of enhancing and reforming the business rates system to support economic growth and long term investment and reflect changing marketplaces. That should never have been of prime importance and we therefore urge the Scottish Parliament to back the measures being put forward by the Minister.”

John Webber, head of rating at Colliers International, added: “The Scottish Government is to be commended for reacting to the Barclay Review so quickly. While English businesses and landlords are still waiting for news on the length or revaluation cycles following recommendations made over a year ago, Scotland has seized the momentum. These measures, especially the move to a three-year revaluation cycle, could have a significant effect in terms of making Scotland more business friendly and encouraging companies to settle North of the Border.

“However, most of these measures will not help businesses in the short term and with continued uncertainty over Brexit the Scottish Government should be encouraged to implement these changes before 2022.”

Scottish landlords and businesses are being warned not to miss the boat to secure fair rateable values, as the appeals deadline looms at the end of September.

Rating experts at Colliers International, the global commercial real estate agency and consultancy, say that following a revaluation that saw double-digit rate hikes in some areas and sectors, it has never been more important for landlords and tenants in Scotland to ensure that the rateable value placed on their property is accurate from the outset.

Louise Daly, associate director of Rating at Colliers International in Scotland, said: “Given the extremely restrictive nature of mid-valuation roll appeals in Scotland, ratepayers have a relatively short opportunity to submit a revaluation appeal and dispute any or all aspects of the valuation that were set from 1st April 2017. They now have less than a month remaining to do so.

“Ratepayers can of course submit their own revaluation appeals within the deadline of 30th September 2017, or they can seek representation to ensure that they are not put at any disadvantage given the complexities of complying with the current appeal system.”

John Webber, Head of Rating at Colliers, added: “Reform of some aspects of the business rates system in Scotland is expected to be soon, including a separate move from Valuation Appeal Committees to a Tribunal system. Ratepayers, therefore, need to stay alert to changes as they happen and ensure that their interests are protected. Lodging appeals now will ensure that any potential validity issues can be resolved- but only just in time. Businesses really cannot afford to delay further.”

Following the Rating Revaluation of 1st April 2017 many businesses have suffered large increases in their business rates. Unlike the rest of the UK, they were given just six months to appeal.

Moreover, despite the recent recommendations made by the Barclay Review panel to move towards a three-yearly revaluation cycle with a ‘tone date’ one year prior to the beginning of the revaluation, nothing has been agreed by the Government to date. Colliers believes that businesses are likely to face another five-yearly valuation cycle at present.

The situation in Scotland is even more precarious because the Barclay Review panel disappointingly did not make any recommendations in respect of the Material Change of Circumstance (MCC) issue north of the border. In Scotland MCC appeals are extremely limited in their scope – a result of High Court decisions made during the period of the 2010 Scottish revaluation cycle. This has made the present appeal system in Scotland much less competitive for ratepayers than in England.

Mr Webber concluded: “Even three-yearly valuation cycles would not go far enough to address specific, localised issues, which in England would have scope for reduction through an MCC appeal. Businesses therefore must not delay. Missing the boat now would be both lengthy and costly.”

Scotland, August 22, 2017 – Following today’s publication of the Barclay Review of Business Rates in Scotland, leading commercial property firm Colliers International is calling on the Scottish Government to implement its recommendations at the earliest opportunity.

Louise Daly, associate director, Rating, at Colliers International in Scotland, said: “The Barclay Review recommendations are clearly an attempt to spread the rates burden more evenly, which would be very welcome to thousands of businesses currently struggling to pay high rates when, at times, their competitors are paying none. We hope the recommendations of the report will be implemented without delay.

“In implementing the recommendations, it is important that the Scottish Government resists the temptation to only focus on any potential revenue raising aspects of this report. It must also give effect to aspects that increase fairness within the system and which help to make it revenue neutral overall. If the Government refuses to give effect to the report fully it will result in a similar outcome to the weak implementation of the Lyons Inquiry of 2007, where certain elements were selected and other ignored. If the Government was to adopt a similar approach it would represent a huge missed opportunity to review the restrictive, outdated and unresponsive rates system.”

Ms Daly said positive aspects of the review include the introduction of a three-year revaluation cycle, with a ‘tone’ date a year prior to be used as a reference for values.

“This provision should be welcomed by all ratepayers, as it instantly makes the system more responsive to changing markets,” she said. “It would be a welcome move from the Scottish Government to exert its devolved powers and lead the way for fundamental changes to the business rates system north of the border. If the Scottish Parliament made changes such as this prior to Westminster, this would be a breath of fresh air, demonstrating that independent decisions can provide a progressive springboard for the rest of the UK to potentially follow the lead of Scotland.”

“From the perspective of responding to changes in the market, more frequent Revaluations are a welcome recommendation. However, it is arguable whether this does go far enough, as the Material Change of Circumstance appeals are now so limited in their scope. As a consequence, Scotland is a less competitive place to do business.

This particular point was put forward by the industry but has not been included within the recommendations. Such omissions are clearly the issue with the scope of the report, as any changes would have to remain revenue neutral.

Another aspect where Scotland currently is less competitive than in England is in respect of the large supplement on the Uniform Business rate. Ms Daly added: “Currently the large uniform business rate is higher in Scotland than in England. It should be reduced and that would be a welcome change to larger property occupiers and investors, but will have to be paid for by other points considered within the report, such as empty property relief applications and potentially large scale commercial processing on agricultural land. Some of these measures will put more pressure on landlords with vacant stock.”

According to Ms Daly, the implications of implementing some of the recommendations with only the view of revenue neutrality could have a significant negative impact on the built and natural environment.

Ms Daly explained: “Removing the 42 days reset period in respect of empty property relief does not encourage landlords to bring their properties back into economic use through means such as short term tenancies. This will actively encourage demolitions to take place, diminishing the property stock.

“Restricting the relief on listed buildings to a maximum of two years and stating that the rates liability for property that has been empty for significant periods should increase is quite dangerous. Listed buildings come with additional costs, due to the nature of the property and any alterations or works that may be required to be carried out. Landlords do not deliberately retain empty property and would much rather have a tenant in place providing an income stream. Limiting relief on such properties could cause them to fall into an uneconomic state of repair. The proposed measures will do little to raise revenue and in the long terms actually work against the incentive of better supporting business growth and long term investment.

“In terms of large scale commercial processing on agricultural land, the distinction needs to be clearly drawn and exactly what type of processing activity specified. It is proposed to do this through consultation and that this will be a long term measure. However, implementing measures such as this with Brexit negotiations taking place should not happen. “

Prime industrial rents for 10-50,000 sq ft units in Scotland have jumped three times faster year on year than the UK average as the lack of building activity forces businesses to compete for available space, according to the latest figures from Colliers International.

The commercial property firm found that prices for prime industrial space rose on average 7.7% in the 12 months to July 2017, compared to a rise of 2.3% in the UK as a whole, to the current Scotland average of £7.59 per square foot (psf). Current UK average is £8.68 psf.

However, the biggest concern is the area around Glasgow, which accounts for much of Scotland’s industrial and logistics needs but is running short of space to accommodate the growth in manufacturing and the retail delivery and distribution segment.

Bo Glowacz, senior research analyst, Research and Forecasting at Colliers International, said: “Availability has been declining gradually year on year in Greater Glasgow to the present 7 million sq ft. The overall vacancy levels have also been falling from 10.2% in 2012 to 8.0%. In terms of quality of the available stock, the vast majority is of poor second-hand quality with only 3% being new and refurbished stock.

“While rental increases have been welcomed by landlords, the Scottish Government’s decision to end 100% rates relief for empty industrial properties last year is likely to restrict speculative going forward, and there are currently no larger buildings planned speculatively in Scotland.

“Indeed, there are virtually no new or nearly new available buildings of between 30,000 and 95,000 sq ft, and just 3 modern warehouses of over 95,000 sq ft currently available, all within Eurocentral.”

Colliers believes that demand for industrial units is being driven by two key factors: the growth of online shopping and therefore delivery and distribution centres; and the recovery in manufacturing which is now accelerating due to the weak pound. Glowacz said that firms that need large units are likely to build their own or have them ‘built to suit’.

“Occupiers have benefited from competitive pricing over the past decade, but rising build costs and higher environmental standards are also placing cost pressure on required rental levels, not to mention empty rates that will now have to be factored into developers’ appraisals. Moving forward, pricing will need to be at new levels for projects to be viable.”

Another Colliers study recently found that the UK has a just over one year’s worth of industrial space left of the market, following a 62% fall in availability since 2009. In Scotland, that figure is closer to 2.5 years after a decline of 44%.

But Iain Davidson, head of Colliers International’s Industrial and Logistics team in Scotland, said that the real lack of available properties at the larger end of the scale posed a problem for the economy. “Many businesses now see modern, good quality premises as a way to operate more efficiently. Having to commission their own new-builds has its advantages as they will get tailor-made facilities, but it is a slower process, which could be a drag on the economy, just as the much-touted manufacturing-led recovery is gaining pace. The Scottish Government should be seeking to encourage commercial building, not placing barriers in its way such as the abolition of rates relief.”

The knock-on effect of Edinburgh’s St James redevelopment has seen prime rents on Princes Street jump by almost a third, according to Colliers International’s 21st Midsummer Retail Report, launched today.

The Colliers International Midsummer Retail Report gives authoritative perspectives across the UK shopping scene by looking at the trends and innovations that are shaping the country’s retail sector and its property market.

Although the current effect is mainly due to the need to find alternative premises for incumbents, after the 1970s shopping centre was demolished to make way for a state-of-the-art replacement, experts at Colliers predict that the £1bn development will give Edinburgh’s retail standing a significant boost when it opens in 2020, by allowing it to compete with Glasgow for big name international retailers.

Colliers’ figures show that the success of Glasgow and Edinburgh helped Scotland post the biggest rise in retail rental rates in the UK, at 4.5%.

Shopping centre completes world city status

• Edinburgh will be able to compete with Glasgow for top retail brands

• Prime space in Edinburgh has increased to £240 per sq ft (up 30%)

• Displacement effect of St James tenants led to latest surge

• Effect will be reversed when centre opens, but less dramatically

• 13th to 8th place in UK Retail Rankings once Edinburgh St James opens

Ross Wilkie, director, retail with Colliers International in Scotland, said: “St James is going to be a world-class shopping centre which, as a destination, is something that Edinburgh has been lacking. The owners already have John Lewis as an anchor tenant but no doubt they may be prepared to offer incentives to get more big name retailers in place ahead of the opening, especially high-end international brands with few UK stores, which can draw footfall from far and wide. So far, many of these retailers have opted for Glasgow’s thriving Buchanan Street area when considering a Scottish store, so the advent of the redeveloped St James should introduce an element of competition.

“In the meantime, rents on Princes Street premises, in particular, have soared as displaced tenants from the old St James battled to secure alternative accommodation. While we may see a reversal when the new St James opens, in the longer term, this will help cement Edinburgh’s credentials as a world city and will be positive for all areas, especially the East of Princes Street, which is closest to the new centre.”

According to the report, Princes Street Zone A rates are back up to £240 per sq ft – an increase of 30% in just two years. Meanwhile Glasgow’s enduring appeal to international retailers continued, most notably in Buchanan Street, which saw a surge in demand and enjoyed corresponding rental growth on the street. In the last 12 months, the Zone A rate has jumped from around £280 per sq ft to a peak of £314 per sq ft.

Prime rents keep on rising

• Scotland has seen the largest rental growth in the UK at 4.5%

• Out of 27 locations, rent has increased in six

• Glasgow has seen prime rents grow 7% to £314 per sq ft

• Stirling (+13%), Aberdeen (+11%), Irvine (+10%) and Dunfermline (+5%) have also increased

John Duffy, director, retail at Colliers International in Scotland, added: “It’s been a busy year for Glasgow’s prime shopping area as retailers compete to secure space in what is currently Scotland’s top destination. H&M has acquired the former 65,000 sq ft Forever 21 store with Victoria’s Secret, Tommy Hilfiger and Calvin Klein all understood to be under offer on back-filling the existing H&M store directly opposite. Other new entrants to the street include Kiko, Hotel Chocolat, T2, Nespresso, Clarks and Swatch.

“For smaller centres, it’s notable that some are still continuing to thrive, showing that it’s largely up to them to reinvent themselves as attractive destinations for shoppers and retailers alike. Retailing has changed in the last decade and we are now seeing a lot of very good multi-channel offerings, and those retailers continue to seek space in the right towns, shopping centres and retail parks to locate their bricks and mortar operations to best complement their online presence.”

“The substantial drop in business rates finally being enjoyed by many retailers in the smaller centres should also provide a boost to those high streets worst hit by the recession. With some areas seeing reductions of up to 70%, there will be more money to invest in bringing both existing businesses and empty properties up to modern standards.”

The Midsummer Retail Report shows that the restaurant market – until recently a booming part of the mix in high streets and shopping centres – has cooled and activity is more selective. The new boom is in ‘drive thrus’, especially following the entry of Canadian chain Tim Hortons into the Scottish market. Other operators active in this market include Costa, Starbucks, McDonalds and KFC.

Duffy continued: “Tim Hortons has given the roadside development market a shot in the arm, with rental levels for drive-thrus and drive-tos being pushed to new rental highs by intense competition in this sub-sector.”

Winners and losers

• Smaller town centres must reinvent themselves to thrive

• Multi-channel retail operations need good locations for bricks and mortar coverage

• Restaurant market remains active but cooled, however ‘drive-thrus’ are booming

The majority of proposed shopping centre development in Scotland is expected to be delivered through extensions. Plans have been approved for the extension of intu Braehead and an extension of Glasgow Silverburn is being planned. The new St Enoch Centre leisure quarter will be a much-needed addition to the southern end of Glasgow city centre.

Meanwhile, the trend towards maximising sales through a multi-channel approach has contributed to around 400,000 sq ft of new retail warehousing space planned to be constructed in Scotland during the next three years. Much of this will come from London & Scottish Investments’ development of former Tesco sites, as well as Ediston’s continuing development of Port Glasgow and other smaller schemes in Fort William and Johnstone.

The significant developments in and around St Andrew Square in Edinburgh are increasing the attractiveness of the east end of the City Centre. The Standard Life Investments and Peveril Securities Development on the south side of St Andrew Square has brought in new occupiers from London in the leisure retail component of the development, namely Dishoom and Drake & Morgan (The Refinery), who opened late last year. Further occupiers anticipated at the end of this summer are Wagamama and Iberica. There is also 100,000 sq ft Grade One office space.

In the south east corner of St Andrew Square, Chris Stewart Group is advancing ‘The Registers’ at the former Royal Bank of Scotland HQ, West Register Street and South St Andrew Street. This will offer 15,000 sq ft of restaurant space, 60,000 sq ft of Grade One offices and 50 serviced apartments.

This area is further supplemented by a new proposal for a £45m concert hall, behind Dundas House at 36 St Andrew Square, for the Scottish Chamber Orchestra. David Chipperfield Architects were appointed in May 2017 to design the 1,000 seat auditorium, which will rival best the best in Europe for acoustics and audience experience.

All of these new developments lie adjacent to the new Edinburgh St James, the TH Real Estate development that is currently being constructed. The 1.7m sq ft development, which will comprise 850,000 sq ft of retail, a luxury hotel, 150 new homes and 30 restaurants, due to be completed in 2020. Next and Everyman Cinemas have agreed pre-lets.

Six-fold rise in Planning fees

Anthony Aitken, head of planning with Colliers International, said: “A new challenge facing retailers and developers in Scotland engaging with the planning system is the new and significant rise in planning application fees. From 1 June, the cost of full applications has increased from just over £20,000 to £125,000 and ‘in principle’ applications now £62,500, up from just over £10,000.

“However, the saving grace is that these remain 50% lower than the English equivalent planning fees.

“Development in the retail core of the Scottish cities often face the multiple challenges of being located within conservation areas and within or in close proximity to listed buildings. These are in addition to the planning application for the development being sought. The engagement with key planning officials to address these multiple challenges can differ from city to city. However, it is the hope of the development industry that the funds raised from the sharp increase in planning fees can assist in providing additional planning staff, which will assist planning departments deliver a high quality and consistent service.”

Rates relief for ailing high streets

• High Streets worst hit by downturn will get the biggest relief following revaluation

• Retailers have seen drop of up to 70% in some locations

• But some pubs and restaurants have seen rates double

The substantial drop in business rates finally being enjoyed by many retailers in the smaller centres should also provide a boost to those high streets worst hit by the recession. With some areas seeing reductions of up to 70%, there may be greater appetite to bring both existing businesses and empty properties up to modern standards.

However, while retailers are seen as the winners in Scotland’s first rates re-evaluation since the recession, many restaurateurs have seen their rates go up.

Louise Daly, senior surveyor, Rating at Colliers International in Scotland, said: “Some landlords will find that properties that they have long struggled to fill are suddenly in demand, due to a substantial drop in rates. Others will be encouraged to invest in their buildings, although that will take a little more time to reflect itself in the market.

“However, with many licensed premises facing a large hike in rates, there is a danger that some pubs and restaurants will be driven out of business and that landlords may then have to seek either a change of use or to convert these units to a configuration more easily adaptable to Class 1 retail. I don’t think that this is happening yet to any great extent, and the cooling of the hospitality property market seen this year is likely to be the result of consumer trends alone. However, we did see such changes of use in the other direction when retailers were being hit with high rates, so the revaluation may yet affect the business make-up of high streets in the coming years.”

Aberdeen

The Midsummer Retail report notes that Aberdeen’s city centre shopping continues to come to terms with the knock-on effect of the oil price drop, which has hit the local economy hard. While occupancy levels having fallen across the city as a whole, prime rates were up 11%, showing that the city is still an attractive venue for many retailers.

John Duffy said: “Rental levels in the very prime pitches – notably Union Square and the Bon Accord Centre – continue to hold up well.”

Dundee

In Dundee, the opening of the £80m V&A Museum in late 2018 will continue to be a catalyst for new development in the city centre. But while the opening of the new museum is expected to dramatically increase tourism numbers and retail spend in the city, there is little sign yet that retailers are jockeying for position.

John Duffy said: “It’s a little too early yet to know exactly how the V&A will affect retail rents, or what further developments will surround it. Retailers appear to be waiting to see what happens.”

In the last year, Dundee saw prime retail rents remain static at c £80 psf Zone A.

Economic outlook for Scottish retailers

Dr Walter Boettcher, research director, economic and property with Colliers International, said:

“The Scottish economy increasingly looks to be buffeted more by the oil price adjustment than by political uncertainty. Hence, Scotland continues to underperform UK benchmarks for consumer spending and disposable income growth – flat in 2016 and forecast to remain weak in 2017.

“Real wage growth is weak due to imported inflation, the result of sterling’s 15% decline after the Brexit vote. In April, real wages were falling at a 1.9% annual rate. Disposable income is also down and house price growth in Scotland remains unsupportive, all of which inevitably affects consumer confidence.

“While this may not augur well for retail performance and rental growth, the Scottish major markets are doing surprisingly well.

“Like other parts of the UK, rental growth has stabilised with positive growth in Glasgow and Edinburgh. Despite these positive signs, there is still a way to go before rents in Scotland’s secondary cities reach the levels achieved in 2008. Nevertheless, a general rebasing of rents looks to be complete, so with a fair wind, retail pitches in Scotland may begin to close the gap with the recovery that has been seen in other parts of the UK.”

Tackling the high points of the Cairngorms in a route that links some of Scotland’s high ski resorts with icons like the Forth Bridge, this year’s Colliers Cycle Ride promises to be as spectacular as it is challenging.

Tackling the high points of the Cairngorms in a route that links some of Scotland’s high ski resorts with icons like the Forth Bridge, this year’s Colliers Cycle Ride promises to be as spectacular as it is challenging.

Dozens of cyclists from the commercial property firm’s offices across the UK joined their colleagues at Colliers International’s teams in Scotland at the start line in Edinburgh this morning, in a bid to complete the gruelling tour and raise thousands of pounds for charity.

The peloton will cross the Forth Bridge and proceed to the River Tay, up to Pitlochry and then into the Cairngorms, following a route that takes in the ski resorts of Aviemore, Lecht and Glenshee.

The Scottish contingent includes veteran riders such as Richard Whitfield, who has already completed five Colliers cycle rides, and first-timers Hannah Murray and Howard Ounsley.

The full Scottish team is:

Ryan Jarvis (2 Colliers Rides to date)

Richard Whitfield (5 Colliers Rides to date)

Jonathan McConnell (3 Colliers Rides to date)

Ian Boxall (2 Colliers Rides to date)

Louise Daly (3 Colliers Rides to date)

Hannah Murray (0 Rides to Date)

Howard Ounsley (0 Rides to Date)

Commercial property specialist Colliers International has prepared and lodged a Planning Permission in Principle (PPP) application for an unusual and ambitious project: the first new prison in the Highlands of Scotland for more than a century.

Commercial property specialist Colliers International has prepared and lodged a Planning Permission in Principle (PPP) application for an unusual and ambitious project: the first new prison in the Highlands of Scotland for more than a century.

The new HMP Highland will replace the 112-year-old HMP Inverness Prison, located in the city centre, with a new 21st century fit-for-purpose prison development.

Working on behalf of the Scottish Prison Service, Colliers International’s planning team lodged the PPP for the new prison facility on land to the south of Inverness Retail and Business Park. As the development proposal represents a technical departure from the Development Plan, Colliers’ work has involved significant pre-application discussions with The Highland Council in addition to the statutory pre-application public consultation.

Meabhann Crowe, Senior Planner at Colliers International, said: “Identifying a suitable site for a new prison facility is a rare task. Finding a suitable location was not as straightforward as with many other buildings. However, the Highlands, Islands and Moray areas need a modern, fit-for-purpose prison facility and we have found an excellent location for the impressive designs, which the Scottish Prison Service has commissioned.

“The new HMP Highland is proposed on a site which we believe to be wholly suitable to this development. It benefits from good accessibility and existing landscaping on the site will assist in creating a setting for the building. The response to the public consultation we carried out was overwhelmingly positive with a complete 100% of respondents in support of the Prison Service’s aim to create a modern, fit for purpose facility.”

Colliers International worked alongside the Scottish Prison Service and a specialist consulting team, including BakerHicks, ITP Energised, Fairhurst Engineers, TGP Landscape Architects, AOC Archaeology and ERM Consulting in bringing the planning application together.

As part of the process, Colliers International’s planning team coordinated pre-application discussions with The Highland Council, statutory pre-application public consultation on 30th March and submission of the overall planning application to The Highland Council on the 25th May 2017. The consultancy team involvement will continue as the application navigates its way through the application process.

Meabhann added: “The consultancy team has worked hard to ensure the proposal is the right development in the right place, and incorporates an exciting design philosophy.”

HMP Highland will serve Highlands, Islands and Moray areas. SPS’ estates strategy involves the commitment to replace historic accommodation with modern facilities which contribute to a Safer Stronger Scotland.

The application is expected to be determined later this year.

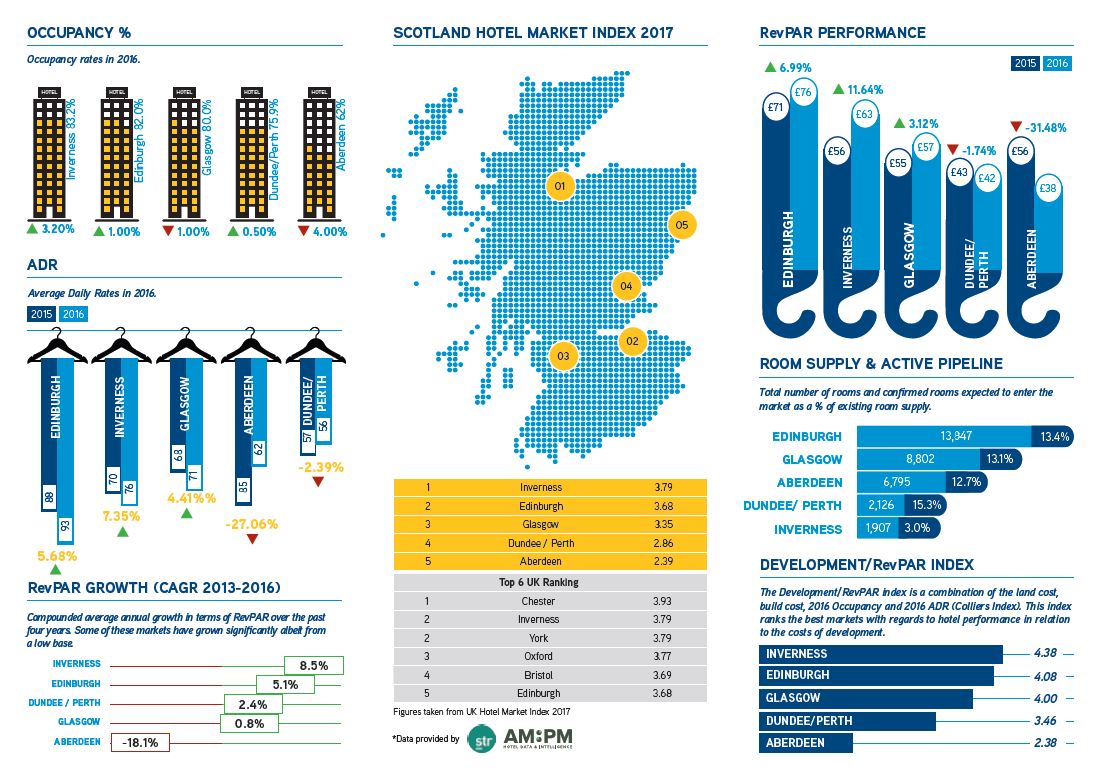

Report ranked five Scottish markets on key points for investors

Report ranked five Scottish markets on key points for investors

Inverness has emerged as the surprise leader in Colliers International’s inaugural Scottish Hotel Index, as a combination of strong levels of demand; rising Average Daily Rates (ADR); a low active pipeline; relatively low development costs and high occupancy levels, allowed it to beat Edinburgh into second place.

Colliers’ Scottish Hotel Index involves the analysis of five locations across Scotland and ranks them according to nine key indicators, to determine the ‘hot spots’ for hotel development and acquisition across the country. It has found that Inverness is the most attractive market for investors, followed by Edinburgh and then Glasgow, Perth and Dundee, and Aberdeen.

Marc Finney, Head of Hotels & Resorts Consulting at Colliers International, said: “Our Scottish Hotels Market Index shows the changes taking place in the sector. The study in particular, highlights that Inverness is not necessarily the best hotel market north of the border, but it is currently providing the best opportunities in Scotland. Inverness has recorded high levels of demand of around 80% over the past four years, which has enabled ADR to rise by 22% between 2013 and 2016. It is cheap to acquire hotel sites there, providing investors with much better value for money than, say, Edinburgh.”

Alistair Letham, the Scottish director in the UK Hotels Agency team at Colliers International, added: “Crucially the index shows that hotel performance is on an upward trend in Inverness, and there is little new stock of guest rooms in development. Despite being expensive, Edinburgh is also on an upward trend and has one of the highest ADR in Scotland and the UK at £93 at the end of 2016. So the capital rightly deserves its position in the UK top ten.”

Highlights

Inverness scored highly and with an overall rating of 3.79, which would put it joint second in the UK, alongside York and behind Chester. Edinburgh is in 5th place in the UK Index.

Inverness led the way in the RevPAR trend, with growth of 8.5%, and also had the highest occupancy rate in the Scottish market with 83.2%.

The city also had some of the cheapest land, alongside Dundee and Perth, and Aberdeen, the smallest active pipeline at under 3% of current room supply, and relatively modest build costs. This allowed Inverness to top the table despite being rated as having only ‘moderate investor appeal’.

Due to data limitations, Dundee and Perth have been analysed as one city, and ranked fourth.

Edinburgh was second with the highest hotel KPIs in Scotland and a ‘very sought after’ investment location, helping it beat Glasgow into third. But its high land price, considerable active pipeline and lower RevPar trend kept it below Inverness for overall investment appeal.

Aberdeen was rated the lowest in Scotland with occupancy rate of 62% and a negative RevPar trend weighing against the Granite City. This is mainly due to the collapse of the oil prices and a large number of new hotel projects.

Mr Finney concluded: “Aberdeen was once the most thriving hotel market in Scotland and the UK but the downturn in oil prices and subsequent offshore activity has hit it hard. It is therefore suffering from a degree of oversupply and tough comparators from previous years. However, that is not to say that it does not have appeal to investors given the market’s potential to improve along with the fortunes of the city’s biggest industry.”

TOP SIX Scottish Hot Spots For Hotel Investment and Development:

1. Inverness

2. Edinburgh

3. Glasgow

4. Dundee/Perth

5. Aberdeen

Methodology

Colliers’ Scottish Hotel Index uses nine Key Performance Indicators (KPIs) to score each of the locations a figure from one to five (one being the lowest and five being the highest). The determining indices include land site prices; build costs; market appetite; valuation exit yields; room occupancy; average daily rate; room occupancy rates; four-year revenue per available room trend (RevPAR); active pipeline as a percentage of current supply and construction costs. The ratings are then consolidated into a single figure and ranked to show the markets that are ‘hot’ and those that are not, in terms of a desirable location for investors to acquire an existing hotel or develop a new one.

Global chain MGM Muthu Hotels, which already has a strong foothold in the UK, has moved into the Scottish market, with the acquisition of five prominent hotels, in a deal facilitated by property firm Colliers International.

Global chain MGM Muthu Hotels, which already has a strong foothold in the UK, has moved into the Scottish market, with the acquisition of five prominent hotels, in a deal facilitated by property firm Colliers International.

The largest deal sees Ian Cleaver’s Highland Heritage Limited sold, from the asking price of offers in excess of £4.5m, to Singapore-headquartered MGM Muthu Group. A former merchant seaman and well-known North West businessman, Mr Cleaver started Highland Heritage in the mid-1970s, and built it into a £8m turnover company, which uses its own fleet of 16 liveried coaches to shuttle tourists to the hotels in Tyndrum, Dalmally and Oban.

The deal, in which Colliers International acted for the seller, comes shortly after the commercial property firm successfully sold another iconic Highland hotel to The MGM Muthu Group, the 63-bedroom Newton Hotel in Nairn. The Newton was once popular with Charlie Chaplin, who took numerous holidays there with his family. It was sold by Colliers on behalf of a London-based corporate owner which was seeking to rationalise its portfolio, and carried an asking price of around £4.0m plus VAT.

Alistair Letham, the Scottish Director in the UK Hotels Agency team at Colliers International, said: “These two sales to a rapidly expanding international operator are a great outcome for everyone involved. Muthu is an ambitious luxury chain which will be well positioned to further develop the potential of these excellent properties in a way that will be welcomed by the local economy. We are pleased to have used our market expertise and international connections to bring about these deals, which see businesses that have invested and grown in the Highlands reap their rewards, and properties move on to the next stage of their history and growth.”

The Highland Heritage Limited sale includes the Volvo coaches and four hotels: the 96-room Royal Hotel, which is a magnet for wildlife, with a masterful touch of stunning views, and the 132-room purpose-built Ben Doran Hotel, nestled in its own sheltered seven-acre garden in the mountain village, on the northern edge of the Loch Lomond National Park, both in Tyndrum. The Dalmally Hotel is a true haven with 99 rooms, commanding breath-taking views in the heart of Strathorchy, perfectly situated to make the most of the historical, cultural and natural delights of Argyll and Bute. The 66-bedroom Alexandra Hotel in Oban, with 26 more rooms in planning, offers gorgeous views across the Oban Bay.

Julian Troup, Head of UK Hotels Agency at Colliers International, commented: “Considerable interest was expressed for the business and assets, which follows a pattern of increasing demand for U.K. provincial hotels. We are seeing an emerging trend of increased demand for quality provincial hotel opportunities from a diverse buyer set, including international investors, who have been attracted by weaker sterling and improving trading prospects; private buyers attracted to the benefits of a lifestyle opportunity to corporate investors attracted to favourable returns and real estate alternatives. Since the beginning of 2016, over 15 per cent of U.K. hotel sales completed by Colliers were to international buyers.”

The MGM Muthu Hotels Group is known for its selection of carefully handpicked spectacular hotels, reflecting the unique character of their destinations, varying from Spain, Portugal, France, Cuba, Canary Islands, Madeira and the UK. MGM Muthu Hotels currently has 27 hotels in their flourishing portfolio, promising excellent service and a touch of home, with a holiday ambience.

Monicca Maran, Corporate Director of MGM Muthu Group and K.Ranjan, CEO of Highgate Asset Management Ltd, who assisted with the acquisitions, said “We are extremely thrilled about the five properties that spell a surreal scenery magically enveloped in the enchanting views of Scotland! Our premium service, excellent standards and charismatic hospitality entwined with the deep appreciation of the historical and cultural landscapes of the hotels will embellish our need to diversify our portfolio, to extend to the community and provide the best holiday experience to all travellers.”

The Highland Heritage sale did not include Kilchurn Castle, the 15th century redoubt of the Clan Cambell on the banks of Loch Awe, which is owned by Mr Cleaver and had been offered for sale alongside his hospitality business. It is currently managed by Historic Scotland.